Agentic AI for Loan Originations: A Secure Architecture for Condition Clearing, Borrower Follow-Ups, and LOS Task Orchestration

2026-05-10

Clarify the condition-clearing workflow your AI will support

Simple condition-clearing loop with ownership and borrower touchpoints

Simple condition-clearing loop with ownership and borrower touchpoints

Agentic AI in loan originations tends to hold up only when the condition-clearing workflow is already defined tightly enough to express as controlled orchestration. Condition clearing is less a single task than a sequence of ownership handoffs, borrower interactions, and LOS state transitions that need to remain coherent under review. When that underlying structure is ambiguous, automation tends to amplify variance, producing uneven borrower experiences and inconsistent evidentiary records. When the structure is well specified, agent coordination can reduce cycle-time drag without diluting underwriting intent or operational accountability.

Condition types and ownership

Mortgage conditions vary by sensitivity, effort, and underwriting impact, and those differences usually map to distinct owners across processing, underwriting, closing, and post-close. Operational predictability often hinges on stable turnaround expectations and a shared definition of “cleared” versus “pending,” expressed through LOS statuses. Misalignment at the status layer commonly drives rework, repeat requests, and avoidable ambiguity during audit review.

Borrower touchpoints and channel approach

Borrower touchpoints often multiply as conditions age, particularly when email, SMS, and portals fall out of sync. A channel approach that concentrates interactions into fewer, clearer exchanges tends to reduce confusion and lower the risk of contradictory instructions. Executive attention typically concentrates on cross-channel consistency, since mismatched messages create operational delay and increase compliance exposure.

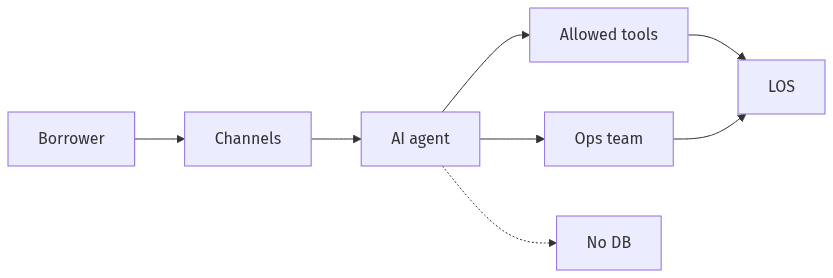

Connect AI to your LOS safely and simply

Bounded AI access through approved tools and controlled LOS updates

Bounded AI access through approved tools and controlled LOS updates

LOS connectivity is a high-leverage—and high-risk—surface area for agentic AI in loan originations. In many lending organizations, the LOS remains the system of record, and its controls, approvals, and separation of duties are expected to remain intact even when orchestration becomes automated. Risk tends to rise when connectivity expands beyond narrowly governed integration points, creating unobserved pathways around existing governance. Executive scrutiny commonly centers on whether integrations remain deterministic, auditable, and reversible under operational and compliance review.

Clear boundaries for what AI can access

Controlled deployments often limit AI to approved tools and explicitly permitted tasks, rather than broad access to underlying LOS data stores. That boundary reduces the likelihood of NPI exposure and narrows the blast radius of errors. Across regulated mortgage operations, action allowlists and role-aware permissions are increasingly used as primary guardrails against unintended agent behavior.

Reliable LOS updates and handoffs

Operational confidence often depends on LOS updates that align with existing controls and remain straightforward to verify after the fact. Handoffs that bypass standard LOS workflows can create shadow operations, leaving downstream teams uncertain about the authoritative task state. Executives typically look for evidence that agent-driven changes are traceable and consistent with established approval paths and exception handling norms.

Protect sensitive borrower data in AI interactions

NPI risk is rarely confined to model prompts; it more often accumulates across logs, integrations, and message content assembled during automated condition clearing. In mortgage operations, data exposure carries regulatory and reputational consequences, with GLBA Safeguards expectations shaping security posture and vendor evaluation. Strong designs treat minimization as a product requirement, not a policy artifact. That stance also reduces the operational friction that surfaces when compliance teams find uncontrolled replication of sensitive data across automation layers.

Share only what’s needed

Field-level minimization often becomes the practical control that keeps AI interactions from inheriting the full borrower record by default. When each action pulls only the attributes required for that decision or message, the risk of oversharing drops. This posture also supports clearer internal accountability, because data access can be explained in business terms rather than defended as technical convenience.

Mask sensitive details and limit storage

Masking and short-lived context reduce the persistence of sensitive information outside systems built for regulated retention. Risk often concentrates in secondary artifacts such as prompt histories, application logs, and message drafts. A bias toward minimal retention narrows discovery exposure and reduces the chance that an “immutable” record becomes an immutable liability.

Keep borrower follow-ups controlled and consistent

Borrower follow-ups are the most visible expression of agentic AI in loan originations, and therefore a common failure mode when messages are inaccurate, inconsistent, or noncompliant. Industry enthusiasm for autonomy often understates the compliance burden of outbound communications, particularly at scale. Mature operating models favor constrained language, stable tone, and policy-bounded content over unconstrained generation. Executive concern typically centers on preventing inaccurate statements, avoiding unfair or misleading language, and maintaining reviewable adherence to channel-consent expectations.

Approved message templates and rules

Template-led communications tend to reduce the risk of incorrect statements, product misrepresentation, or inconsistent disclosures across loan types and jurisdictions. Rules layered onto templates commonly constrain wording by locale and product, limiting drift into impermissible claims. This constraint-first posture also yields cleaner audit artifacts, since reviewers can reconcile outbound content to an approved corpus.

Consent, opt-out, and timing expectations

Automated SMS follow-ups carry heightened sensitivity because TCPA-linked consent and opt-out records can become dispositive in disputes. Channel-preference routing and timing boundaries often determine whether automation is experienced as coordination or as unsolicited pressure. Proof of consent, together with a reviewable opt-out trail, commonly functions as the linchpin for executive comfort with scaled outbound automation.

Maintain reviewable records and human oversight

Reviewable records with approvals for higher-risk actions

Reviewable records with approvals for higher-risk actions

Auditability and human oversight often separate agentic experimentation from production-grade mortgage operations. The regulated nature of loan processing converts many automation questions into evidentiary questions: what occurred, why it occurred, who authorized it, and what data informed the outcome. Governance is frequently asserted at a high level, while operating confidence depends on granular, correlated records that hold up across systems and over time. Human-in-the-loop checkpoints remain central at high-risk moments where uncertainty, exceptions, or sensitive communications raise the cost of error.

Audit-friendly records of key actions

Reviewable records typically extend beyond message content to include decision context, approvals, and downstream system updates. Correlation across the LOS, borrower portals, and communications channels often determines whether an audit trail is explanatory or merely extensive. Immutable logging, treated as evidentiary recordkeeping rather than debugging output, supports defensible accountability for agent-driven actions.

Approvals for higher-risk steps

Human oversight typically concentrates where borrower impact and compliance exposure are highest, including exceptions, ambiguous conditions, and sensitive outbound messaging. Escalation under uncertainty operates as a risk control that preserves throughput without normalizing silent errors. This balance also supports segregation of duties, since approvals can reflect role boundaries even as orchestration becomes more automated.