Alex Fesak

CEO

AI-Powered Accounts Receivable Cash Application for US Fintech: Matching Logic, Exception Workflows, and Controls That Auditors Accept

2026-05-17

Set clear goals and guardrails for automated cash posting

AI-powered cash application in fintech is more reliable when automation targets sit alongside explicit guardrails that prevent low-quality entries from reaching the general ledger. In regulated environments, the definition of “done” extends beyond a higher straight-through rate to defensible records: what was received, what was matched, why the system considered the match valid, and who approved exceptions. Those expectations shape risk tolerance for autonomous behavior, particularly where SOX-aligned controls and segregation of duties determine what can post automatically versus what remains subject to review.

Success metrics that matter

Finance leadership typically focuses on measures that map directly to the close: auto-match rate, match accuracy, unapplied cash aging, and the cycle time from deposit to posting. Targets usually vary by payer segment and remittance channel, since EDI/ERA inputs tend to normalize more consistently than email PDFs or lockbox images.

Common risks to plan for

The main downside of automation in cash application is error scale: false-positive matches, incorrect split allocations, and misclassified deductions can drive disputes and manual rework downstream. Control weaknesses also surface as audit findings, especially when system changes, model updates, or privileged access lack traceable evidence and oversight aligned to SOX 404 expectations.

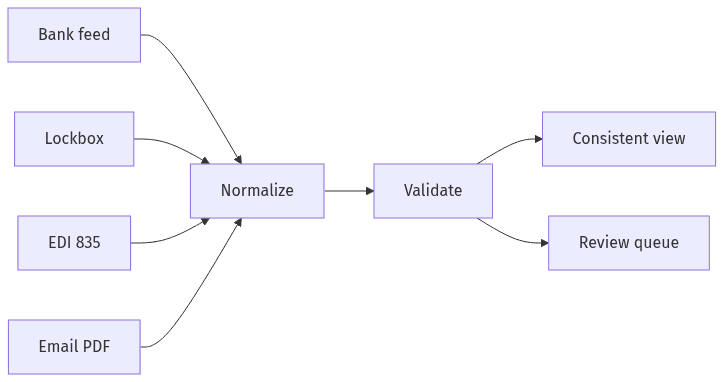

Bring remittance inputs into one consistent view

Remittance inputs normalized into one consistent view

Remittance inputs normalized into one consistent view

Cash-application reliability often tracks input consistency more than matching sophistication. In many US fintech AR teams, payment channels run concurrently—ACH, wire, card, and lockbox—while remittance arrives as EDI X12 835, portal exports, email bodies, and attached PDFs. The operational constraint is normalization: payer identity, invoice references, and amounts need a coherent representation before matching decisions stabilize. Without that consistency, confidence scoring tends to swing, and unapplied cash accumulates as exceptions rather than declining.

Quality checks and reconciliation basics

Audit scrutiny commonly centers on completeness and existence: whether remittance inputs reconcile to bank deposits and whether critical fields are present and plausible. Validation expectations typically cover payer identifiers, payment amounts, currency, dates, and traceable links between lockbox deposits or bank activity and the remittance record retained for later examination.

Use safe matching decisions that reduce unapplied cash

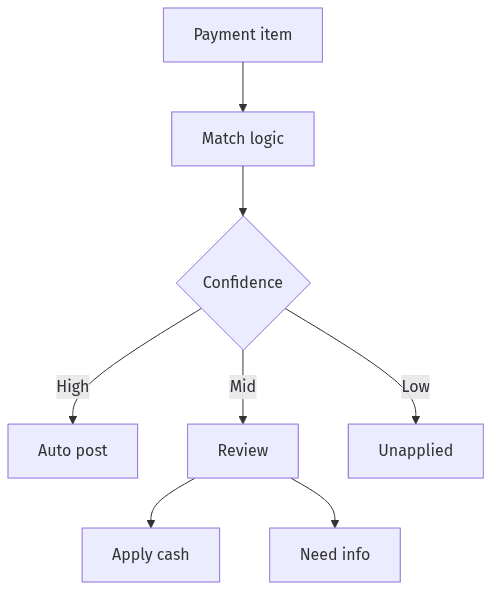

Confidence bands guide post, hold, or review

Confidence bands guide post, hold, or review

Automated matching in AR often settles into a hybrid of deterministic logic and probabilistic scoring, with the core tradeoff between straight-through processing and posting risk. Deterministic rules usually anchor on strong references such as invoice number and exact amount, while ML-style scoring helps interpret weaker signals such as payer name variance and memo text. Treating confidence scores as correctness tends to draw auditor skepticism, so emphasis shifts to conservative thresholds, predictable fallback behavior, and a clear separation between cash posting and adjustment treatment.

Match priorities and confidence levels

Matching outcomes typically fall into bands that govern whether items post, hold, or escalate: high-confidence matches with strong references, mid-confidence items requiring review, and low-confidence items treated as unapplied cash. Priority ordering commonly favors unique identifiers and exact totals before considering partial references or fuzzy payer-to-customer mappings.

Handle deductions and payment differences

Short pays, deductions, and chargebacks introduce policy sensitivity because they blur the boundary between cash receipt and dispute or adjustment accounting. Many programs maintain a deliberate distinction between “clean cash” items suitable for automated application and variance items that require categorization, evidence capture, and consistent treatment to reduce silent margin leakage.

Manage exceptions with clear ownership and approvals

Exception workflows often determine whether automation reduces manual work or relocates it into review queues. In fintech environments, unmatched payments, ambiguous invoice references, and deduction-heavy customers create a steady stream of items that require clear ownership and response expectations across AR operations, billing, and sometimes support. Governance matters because the most material control exposure concentrates in exception handling: manual overrides, write-offs, and adjustments are the points most susceptible to error or misuse and therefore draw the highest auditor attention.

Routing and escalation expectations

Exception categories generally stabilize into a taxonomy that supports accountability: unknown payer, missing invoice reference, partial payment, deduction, and multi-invoice ambiguity. Operational transparency depends on consistent ownership and resolution tracking, since aging exceptions often correlate with unapplied cash growth and delayed close activity.

When overrides need approval

Higher-risk outcomes usually trigger sign-off expectations, particularly for write-offs, unusual allocation changes, and postings that diverge from remittance totals. Auditor-ready operations typically treat overrides as controlled events, with recorded rationale, linked evidence, and visible approver identity to support segregation of duties and retrospective review.

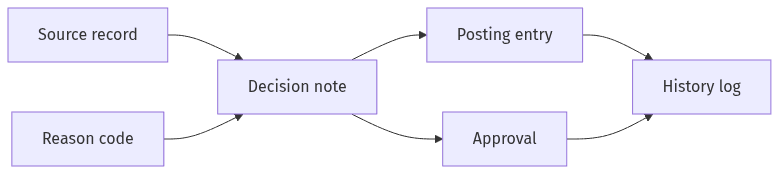

Keep decisions easy to review and ready for audits

Decision records connect inputs, outcomes, and approvals

Decision records connect inputs, outcomes, and approvals

Audit acceptance of AI-powered cash application often depends less on model sophistication than on reviewability: a clear account of why a match occurred, what information supported it, and what changed between initial ingestion and final posting. Explainability generally takes the form of durable reason codes, retained source artifacts, and immutable logs that connect remittance, invoice selection, applied amounts, exceptions, and approvals. That evidentiary chain supports internal control narratives aligned to COSO concepts and reduces perceived “black box” risk.

Decision notes that explain outcomes

Explainable matching typically appears as structured decision notes: the fields used, the confidence score or rule trigger, and the reason codes that justified application versus hold. Review is more straightforward when before-and-after values exist for allocations, adjustments, and overrides, giving control testing objective evidence.

Recordkeeping and access discipline

Recordkeeping discipline typically centers on retention, tamper resistance, and fast retrieval across the remittance-to-posting chain. Access patterns draw comparable scrutiny, since privileged ability to alter matching rules, confidence thresholds, or posted entries can weaken segregation of duties and complicate SOX testing without clear change history and approval evidence.