Alex Fesak

CEO

AI Underwriting Conditions Triage for US Mortgage Teams: Build vs Buy, Secure Architecture, and a 30-Day Pilot Plan

2026-05-24

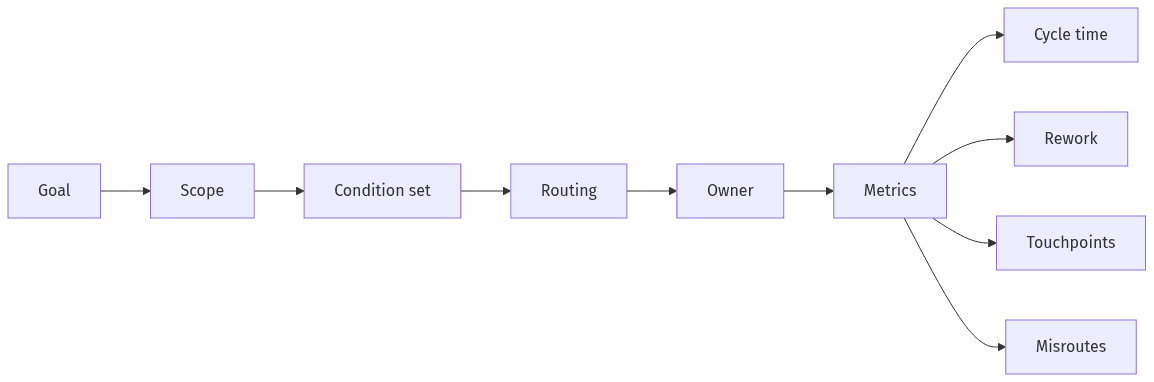

Clarify the triage goal and success measures

Triage goal to metrics mapping

Triage goal to metrics mapping

AI underwriting conditions triage tends to hold up when the objective stays narrow and measurable: faster condition clearance, fewer misroutes, and fewer borrower touchpoints. In many lending organizations, the binding constraint is less model performance than agreement on what constitutes improved throughput, quality, and borrower experience. The most decision-useful framing treats triage as condition classification and normalization, routing to the appropriate owner or queue, and coordinated borrower requests and reminders, with cycle-time and rework outcomes evidenced in LOS events and communication records.

Current performance snapshot

A useful snapshot typically centers on underwriting cycle time, queue aging, handoffs between underwriting and processing, rework frequency, and routing accuracy. Across many lenders, these signals already exist in LOS timestamps and notes, task and assignment history, and email/SMS records; those same sources often surface duplicate borrower follow-ups and inconsistent condition descriptions that undermine reporting.

First-use scope for triage

Initial scope commonly concentrates on a limited set of frequent condition types where classification ambiguity and repeated borrower follow-ups are most apparent. High-volume conditions also produce enough data for measurement within a short window, while keeping underwriter confidence higher because the triage boundaries remain explicit and the operational surface area stays contained.

Decide build vs buy for mortgage operations

Build-versus-buy decisions in mortgage operations rarely turn on feature checklists alone; they turn on time-to-value, security review friction, and long-term ownership cost. Buying typically concentrates risk in vendor due diligence and integration fit, while building concentrates risk in ongoing maintenance, model governance, and the internal burden of keeping workflows stable as LOS configurations and compliance expectations shift. Executives often compare these paths through cycle-time impact, auditability, Encompass compatibility, and whether ROI evidence is credible within a pilot timeframe.

When buying is the better fit

A vendor platform often fits lenders prioritizing near-term cycle-time reduction and lower initial operational burden, particularly when SOC 2 Type II expectations or procurement timelines are gating factors. Reference quality often becomes the differentiator, since “mortgage-ready” claims vary in condition taxonomy depth, controls for touchpoint deduplication, and the availability of routing evidence that supports review.

When building is the better fit

A custom build commonly fits organizations with idiosyncratic condition language, specialized routing rules, or internal governance constraints that require direct control. The trade-off typically appears as sustained ownership: managing behavior drift, keeping audit logging consistent, and absorbing the backlog associated with integrations and exception handling as operational policies change.

Keep workflows safe, secure, and reviewable

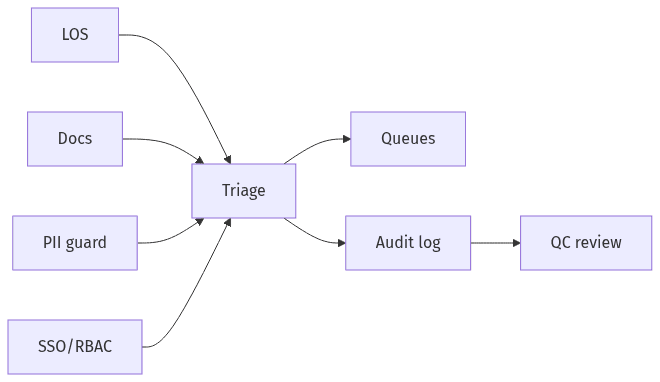

Secure, reviewable triage around existing LOS

Secure, reviewable triage around existing LOS

Condition triage touches borrower PII and sits adjacent to decision-critical operations, so security and reviewability often govern adoption more than model accuracy. Across regulated mortgage operations, confidence is higher when triage outputs remain transparent, attributable, and straightforward to audit, rather than framed as opaque “AI decisions.” Designs that tend to endure prioritize minimal disruption to LOS-centric workflows (often Encompass), strict access boundaries, and durable evidence trails that align with GLBA safeguard expectations and record-retention realities without creating an unreviewable black box.

Integration approach that minimizes disruption

Operational stability tends to improve when triage aligns to existing LOS tasks, queues, and status changes rather than adding new user-interface surfaces. In many organizations, the practical requirement is continuity: underwriters and processors remain in familiar handoffs while triage outputs appear as standardized condition descriptions and routing signals that fit established workflow conventions.

Privacy and access safeguards

LLM risk reviews frequently focus on PII exposure through prompts, logs, and vendor data-retention practices, not solely on model accuracy. Common safeguards include PII redaction and data loss prevention, role-based access control with SSO, and audit logs that preserve what was routed and the rationale, while limiting unnecessary sensitive-data propagation and supporting governance and recordkeeping expectations.

Include human review and clear exceptions

Human review gates and exception handling

Human review gates and exception handling

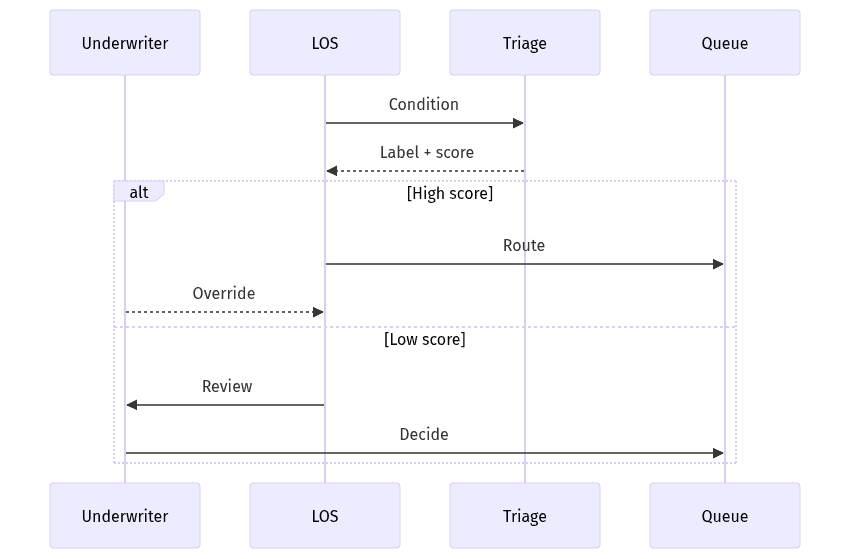

Mortgage underwriting remains accountability-heavy, so human-in-the-loop review often determines whether triage is trusted across underwriting and processing. The practical aim is not autonomy; it is reducing avoidable rework while keeping underwriter override authority intact. Confidence scoring and exception categories often become the shared operating language because they set expectations for when triage can normalize and route conditions consistently and when edge cases should be held for review. Auditability and explainability reinforce this by keeping routing outcomes defensible during QC and governance review.

Review gates and escalation paths

Reviewability improves when triage outputs include clear confidence signals, standardized labels, and explicit fallbacks that preserve continuity in underwriting ownership. Underwriter overrides remain central to credibility, and exception handling reduces operational risk from hallucinations or misclassification by surfacing ambiguity for review rather than silently routing it.

Run a 30-day pilot and decide next steps

A 30-day pilot tends to perform best as a procurement-grade proof point: narrow scope, fast measurement, and a go/no-go outcome tied to cycle time and touchpoint reduction. Leaders typically expect weekly visibility into routing accuracy, rework rates, borrower contact volume, and throughput impact, with thresholds defined up front to limit post-hoc interpretation. In many pilots, measurement clarity is more decisive than model sophistication, particularly when baseline LOS events and communication records provide objective comparators for operational load and borrower experience.

Pilot plan and weekly checkpoints

Weekly checkpoints typically stay anchored to a small condition set, stable workflow boundaries, and tracked KPIs such as cycle time, routing accuracy, rework rate, and borrower touchpoint counts. LOS event baselines and communication logs usually provide the most defensible signals, while scope discipline helps prevent results from being confounded by unrelated operational variability.

Scorecard and go/no-go decision

A decision-ready scorecard typically summarizes KPI deltas, security and privacy findings, integration stability, and governance readiness, alongside residual risks such as duplicate messaging and gaps in routing explainability. Procurement-facing artifacts often highlight SOC 2 Type II posture, GLBA-aligned safeguard expectations, audit logs and evidence retention, and an explicit delineation of what remains human-reviewed versus automated.