Stripe vs Adyen vs Braintree for US eCommerce: A Solution Architecture Comparison for Subscriptions, Fraud, and Multi-Entity Reporting

2026-05-04

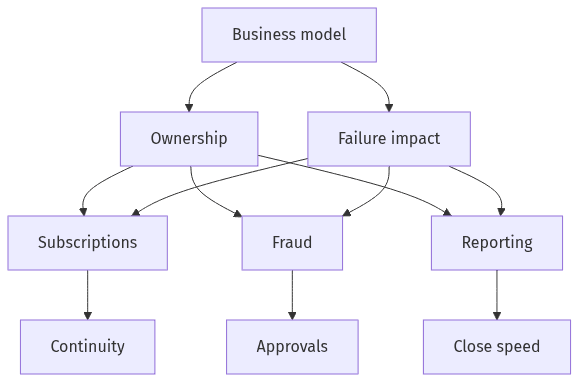

Choose based on your business model and risk appetite

Platform fit tradeoffs across revenue, risk, and finance

Platform fit tradeoffs across revenue, risk, and finance

In US eCommerce, Stripe vs Adyen vs Braintree comparisons often default to feature checklists, yet platform fit more often hinges on operational ownership and the business impact of failure modes. Subscription-heavy revenue models increase sensitivity to dunning behavior, proration logic, and event delivery reliability, while multi-brand and multi-entity structures elevate settlement attribution and finance-grade reporting as core selection criteria. Risk appetite similarly shapes outcomes: aggressive approval optimization, conservative fraud posture, and dispute handling maturity each introduce distinct tradeoffs across tooling, workflow design, and data visibility.

What matters most in your scenario

Priorities often cluster around three executive concerns: revenue continuity in recurring billing, loss containment without excessive false declines, and reconciliation speed across legal entities. Capabilities matter less than clarity on expected outcomes, internal accountability for payment events end-to-end, and tolerance for differences in reporting semantics for fees, refunds, disputes, and payout grouping.

Subscriptions: revenue stability and customer experience

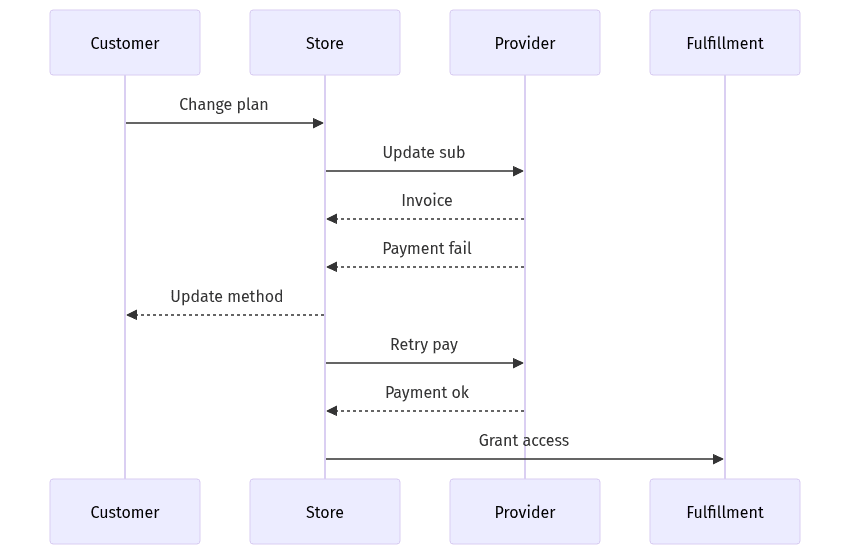

Subscription change and retry loop touchpoints

Subscription change and retry loop touchpoints

Subscriptions turn payment infrastructure into a recurring customer experience, which makes processor selection meaningfully different from one-time checkout optimization. Stripe Billing, Adyen’s recurring capabilities, and Braintree subscriptions each model subscription states, invoices, retries, and credits with different semantics that become visible during migrations, pricing changes, or catalog restructuring. The most consequential differences tend to surface in edge cases: partial-period proration, mid-cycle upgrades and downgrades, pause and resume behavior, retry cadence, and how payment failures propagate into fulfillment and entitlement systems through webhooks and event feeds.

Retries and dunning outcomes

Recovery performance depends on whether retry attempts, dunning communications, and payment method updates map consistently to subscription status and ledger impact. Involuntary churn often increases when retry behavior changes during a processor transition or when event uncertainty creates gaps between billing state and downstream order state, even when payment attempt history exists in the processor.

Plan changes and billing accuracy

Billing accuracy becomes a finance issue when upgrades, downgrades, credits, and cancellations produce inconsistent invoice calculations or unclear revenue attribution across entities. Differences in how platforms represent proration, adjustments, and invoice finalization can complicate parity assumptions and introduce audit friction when historical subscription periods no longer align cleanly with reported charges and refunds.

Fraud and disputes: approvals, losses, and operational load

Fraud tooling comparisons across Stripe Radar, Adyen RevenueProtect, and Braintree risk features often emphasize rule sets, yet the operational concern is the combined effect on approvals, chargebacks, and review workload. False declines can carry higher lifetime cost than fraud losses during growth phases, while mature brands often rebalance toward brand protection and dispute throughput. Platform differences also show up in how risk signals and manual review context attach to payment lifecycle events, shaping how consistently operations teams interpret declines, holds, refunds, and subsequent disputes.

Risk controls and review workflow

Ongoing optimization tends to depend on signal transparency, decision stability, and the ability to correlate risk events to downstream revenue and support contacts. Rule tuning is usually constrained less by control availability than by measurement clarity, particularly when multiple brands and entities share traffic patterns but require distinct risk postures.

Disputes and chargeback handling

Dispute operations often suffer from cross-platform inconsistency: status definitions, evidence packaging, representment timelines, and reporting fields vary in ways that complicate portfolio-level tracking. Standardized measurement becomes harder when dispute objects and reason codes lack parity across providers, obscuring whether outcome shifts are driven by fraud policy changes, customer support behavior, or processor handling.

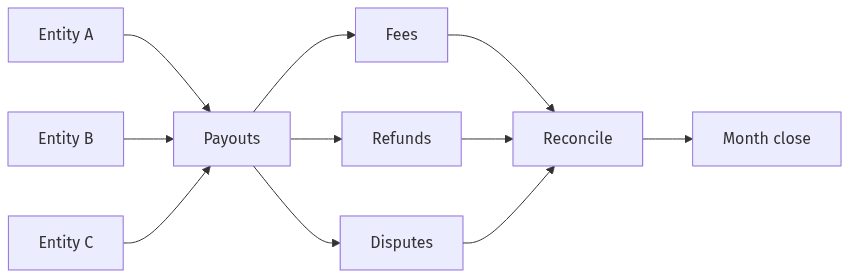

Reporting and reconciliation across entities

From payouts and fees to month-end close

From payouts and fees to month-end close

Multi-entity reporting separates finance-ready payment operations from basic gateway integrations, because payouts and fees ultimately feed close, audit support, and margin analysis. Stripe balance transactions, Adyen settlement details, and Braintree reporting exports each provide different levels of granularity and attribution for fees, refunds, disputes, and adjustments. A recurring friction point appears when legal entity boundaries, brand hierarchies, and payout groupings do not match internal ledger expectations, pushing finance teams into manual reconciliation and extending month-end close while increasing audit exposure.

Payouts and fee visibility

Reconciliation confidence depends on whether each charge, refund, dispute, and fee can be traced to a specific payout and entity without ambiguous aggregation. Gaps often show up in fee allocation, timing differences between authorization, capture, refund, and settlement, and inconsistent representations of adjustments that complicate double-entry alignment.

Exports for finance and analytics

Export characteristics often become decisive when BI, accounting, and audit requirements converge. Finance-grade pipelines rely on stable identifiers and consistent field meaning over time, yet provider exports vary in normalization depth, join paths across lifecycle events, and metadata completeness needed to tie payment objects back to orders, subscriptions, or entities.

Switching providers without disrupting revenue

Processor migrations create a concentrated risk window in which subscription continuity, dispute backlog handling, and reconciliation parity can fail in parallel. Recurring misconceptions—such as treating webhook delivery as certain or assuming subscription token portability—create hidden exposure when event schemas, identifiers, and lifecycle semantics change underneath existing commerce logic. Migration outcomes tend to track the ability to maintain event-driven correctness and observability during the transition, since missed payment events more often surface as missing orders, missing refunds, fulfillment drift, and delayed close issues than as immediate checkout failures.

Cutover approach and customer impact

Customer-visible disruption often emerges through billing timing shifts, unexpected authentication prompts, and inconsistent retry behavior that resembles product instability. Sensitivity is highest in recurring billing cohorts, where a single missed event or mismatch in subscription state can cascade into entitlement errors and service interruptions that increase support volume and elevate churn risk.

Validation and operational readiness

Confidence during a switch rests on parity expectations across charges, refunds, disputes, and payout attribution, with observability serving as the early-warning layer for failures that do not surface at checkout. Operational load also changes during migrations as teams reconcile differences in dispute status semantics, reporting exports, and webhook or event sequencing, and those differences can persist after cutover into routine finance and risk operations.