Build vs Buy: Mortgage LOS Integrations for Faster Underwriting (Encompass, Empower, and Point-of-Sale Systems)

2026-04-19

Find the biggest underwriting slowdowns caused by system handoffs

Where handoffs create rework and SLA misses

Where handoffs create rework and SLA misses

Underwriting cycle-time slippage often traces to handoffs between the mortgage point-of-sale platform, the loan origination system (LOS), and downstream underwriting tools. In Encompass and Empower environments, the most visible symptoms are stalled file movement, mismatched loan statuses, and repeated clarification when teams rely on different “sources of truth.” Operationally, the gaps show up as SLA misses and extra touches, not a single failed integration. Executive clarity tends to improve when delays are described as handoff latency, data drift, and exception volume rather than vendor fault.

Identify the workflows that matter most

The workflows with the highest underwriting impact usually cluster around milestone status movement, document conditions, and ownership transitions between sales, processing, and underwriting. A recurring pattern occurs when turnaround expectations depend on timely milestones and complete files, yet updates arrive late, land out of sequence, or differ by system. The practical outcome is queue volatility and avoidable rework that cannot be cleanly attributed to one team or one platform.

Surface common points where connections fail

Breakdowns often surface after LOS releases, connector updates, or gradual shifts in field usage. Integrations can appear “up” while silently drifting, producing partial or inconsistent updates that trigger manual correction and rekeying. Post-release incidents also tend to expose an ownership gap, where root-cause analysis spans multiple vendors and support boundaries are not explicit.

Clarify what information must move between systems

High-value signals across POS, LOS, and docs

High-value signals across POS, LOS, and docs

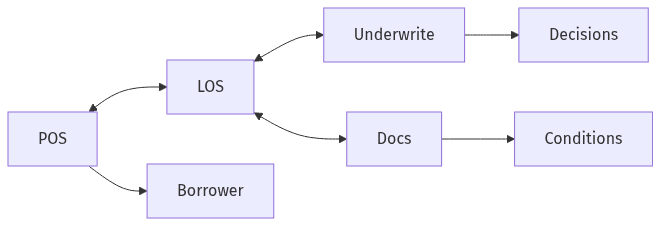

Mortgage LOS integrations typically succeed or fail on information fidelity, not on whether an interface exists. Underwriting velocity depends on a narrow set of high-value signals: status changes that represent actual progress, fields that remain aligned across systems, and documents that arrive with the metadata needed for conditions clearance. Confusion tends to emerge when “real-time” is assumed to mean parity, even though platforms represent timing, milestones, and field semantics differently. Clear expectations for timing, completeness, and system-of-record authority reduce downstream ambiguity.

Status updates and visibility expectations

Status visibility matters most at milestone transitions, where underwriting capacity planning and borrower communication depend on accuracy. A recurring misconception is that near-instant updates should exist for every event, despite operational realities such as delayed sync, dropped messages, retries, or inconsistent milestone definitions. Reliable visibility depends on timeliness plus a credible reconciliation backstop when discrepancies occur.

Document sharing and completeness needs

Document exchange issues commonly show up as missing conditions, duplicate uploads, or files arriving without consistent indexing and traceability. Underwriting teams experience this as file-completeness exposure, while operations experiences it as repeated follow-up and cycle-time drag. Auditability becomes material when file contents cannot be reliably traced across the POS, LOS, and imaging repositories.

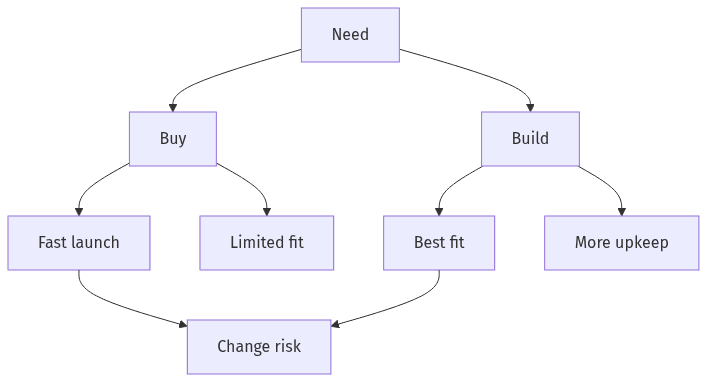

Choose build vs buy based on speed, fit, and change risk

Build vs buy tradeoffs over time

Build vs buy tradeoffs over time

The build-versus-buy decision for mortgage LOS integrations tends to hinge less on vendor preference and more on change cadence and workflow specificity. Packaged connectors generally prioritize fast availability for common patterns, while custom API integration is often selected for adaptability when underwriting automation, nuanced milestone logic, or specialized document handling sits at the core of the operating model. Change risk is the differentiator that accumulates over time: LOS updates, API version shifts, and evolving field usage can turn early speed into recurring disruption. Most decisions balance delivery speed, fit, maintenance load, and support accountability.

When packaged connectors are enough

Packaged connectors often fit environments where required milestones and document movement map cleanly to marketplace options. Their appeal usually centers on shorter implementation horizons and simpler contracting, especially for baseline LOS-to-POS synchronization. The trade-off often appears later as constrained flexibility when workflows evolve or when connector behavior lags LOS release cycles.

When custom work is worth it

Custom work is typically justified when underwriting automation relies on specific triggers, field-level validation, or differentiated borrower and operations experiences. The long-term benefit is tighter control over data semantics and the ability to adapt as product, compliance, or operational priorities shift. The counterweight is sustained ownership for upgrades, monitoring, and ongoing compatibility with Encompass or Empower change cycles.

Estimate timeline and long-term effort beyond launch

Timeline discussions around mortgage LOS integrations often emphasize initial delivery, yet integration durability drives total cost of ownership. Post-launch realities commonly include field mismatches, version changes, connector regressions, and operational overhead tied to incident triage and partner coordination. The executive risk is gradual erosion: rework accumulates and optimization is deferred, so underwriting gains taper over quarters rather than failing at a single visible point. Delivery duration is also shaped by access constraints and change-control dependencies outside the integration team’s direct control.

What drives ongoing cost over time

Ongoing cost concentrates in maintenance: absorbing LOS platform updates, correcting data defects that surface as operational rework, and sustaining monitoring and support coverage. Hidden effort typically appears as exception handling, manual corrections, and multi-vendor coordination when responsibility boundaries are unclear. Over time, this can exceed the original integration lift, particularly when “stable fields” are redefined or repurposed.

What commonly slows delivery

Delivery drag commonly stems from environment access, security approvals, vendor change windows, and cutover constraints tied to business calendars. Testing limits and sandbox availability can compress validation, increasing downstream defect exposure. Dependencies on third-party vendors for issue resolution add schedule uncertainty, especially when an incident spans the POS, LOS, and document systems.

Make reliability and data protection part of the plan

Reliability and data protection function as underwriting performance controls, not only technical concerns. Across mortgage operations, instability becomes operational churn: missed status events, incomplete files, and manual rekeying that undercuts automation. Data protection carries parallel weight because borrower PII and documents traverse multiple platforms, each with distinct access models and audit expectations. Regulatory pressure, including GLBA Safeguards Rule considerations and evolving state privacy laws, raises the cost of ambiguity around accountability. Durable integrations typically reflect explicit fault-tolerance expectations and disciplined cross-vendor change management.

Baseline expectations for protecting borrower information

Borrower data handling expectations generally include controlled access, clear accountability for data sharing, and consistent auditability across systems. Risk concentrates when integrations expand the footprint of sensitive data without consistent logging, retention discipline, and oversight. Compliance scrutiny often increases when document movement and indexing reduce traceability, or when data is replicated across platforms without a defined governance rationale.

Operational readiness for ongoing stability

Operational readiness shows up in the ability to detect failures quickly, distinguish data defects from platform incidents, and coordinate resolution across internal teams and vendors. Upgrade resilience is a recurring theme in Encompass and Empower ecosystems, where platform updates can change behavior even when interfaces remain nominally available. Stability tends to correlate with monitoring coverage, explicit support ownership, and consistent change-control expectations.