Alex Fesak

CEO

Mortgage Lead-to-Loan Funnel Automation with AI: A Secure Blueprint for Intake, Eligibility Triage, and Borrower Outreach (Without Replacing Your LOS)

2026-05-22

Set funnel goals and guardrails

Mortgage lead-to-loan automation commonly succeeds or stalls based on clarity around outcomes and boundaries, not model capability. Executive attention typically centers on speed-to-contact, reduced fallout during intake and document collection, and improved pull-through into a completed application, while risk stakeholders focus on durable borrower-consent evidence and containment of PII consistent with GLBA expectations. A credible “secure blueprint” narrative also depends on explicit non-goals, including avoiding any implication of LOS replacement and keeping approvals from widening into an open-ended transformation program.

Pilot success measures

Pilot measurement usually concentrates on baseline-versus-week-by-week shifts in contact speed, missing-document fallout, and conversion from lead to application. Funnel ROI narratives in mortgage operations typically hinge on reduced manual rework, fewer stalled files, and lower follow-up volume, with metrics accompanied by definitions that remain stable across CRM, POS, and LOS reporting views.

Scope and owners

Cross-functional ownership commonly becomes the determinant of cycle time, particularly when compliance review, vendor risk management, and IT integration work proceed in parallel. A tight scope generally reflects explicit responsibility boundaries between lending operations, technology, and compliance, along with limits that prevent expansion into underwriting policy, pricing logic, or core LOS processing.

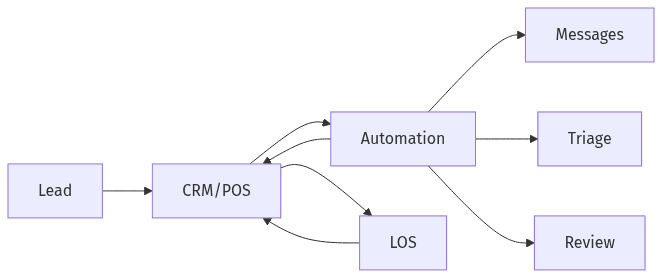

Design an automation layer that works with your LOS

Automation layer supports CRM/POS while LOS stays system of record

Automation layer supports CRM/POS while LOS stays system of record

Across mortgage operations, a layered stack is already the norm: lead capture and engagement in CRM/POS, with authoritative loan records maintained in the LOS. AI lead-to-loan funnel automation typically fits as an orchestration layer that coordinates intake, eligibility triage, and borrower outreach while preserving the LOS as the system of record. The executive decision lens often emphasizes non-invasive integration patterns, predictable data ownership, and a borrower experience that remains coherent even when different systems control different stages of the journey.

Core systems and touchpoints

System boundaries typically separate early-stage engagement data from loan-file truth, with CRM/POS carrying lead source, consent, and activity history while the LOS retains regulated loan artifacts and underwriting status. Non-invasive LOS interaction commonly aligns with limited write-backs or status updates rather than attempting to mirror or replace LOS workflows.

Reliable handoffs and tracking

Funnel automation frequently breaks down at handoffs, where duplicate outreach, missed follow-ups, or contradictory status signals erode borrower trust and elevate compliance exposure. Reliability discussions often focus on event-driven synchronization, consistent identifiers across systems, and observable activity trails that reconcile what was communicated with what the systems recorded.

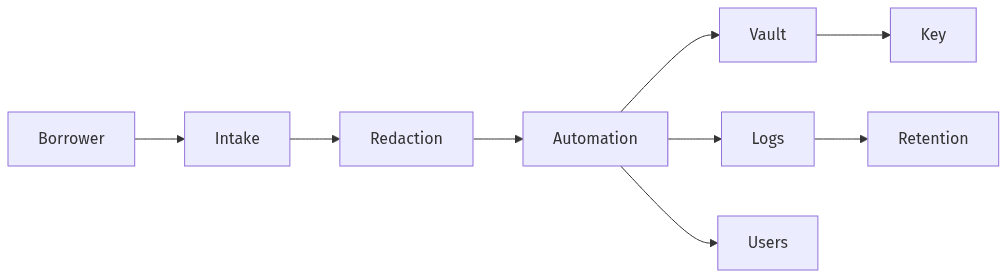

Protect borrower data from day one

Minimize data use with controlled access and short retention

Minimize data use with controlled access and short retention

Security posture becomes a primary selection criterion when AI agents touch borrower intake, documents, and communications. Mortgage funnels carry concentrated PII and sensitive financial attributes, and the risk surface often extends beyond databases into prompts, logs, message archives, and third-party tooling. A security-first blueprint typically frames data minimization as an architectural constraint rather than a policy slogan, aligning with governance expectations reflected in SOC 2 controls and risk-based frameworks such as NIST AI RMF, without implying blanket safety by default.

Where sensitive data can leak

Leakage risk often appears in unredacted conversational context, diagnostic logs, monitoring dashboards, and vendor support tooling, particularly when troubleshooting becomes routine during pilots. The governing theme across these surfaces generally centers on least-possible exposure, with only the minimum borrower attributes present for a given funnel decision.

Access, retention, and records

Audit readiness and incident-response posture often depend on access boundaries, shortened retention, and evidence of key actions rather than broad data hoarding. Across regulated lending environments, programs typically maintain defensible records of consent, communications, and status changes with clear retention logic, while sharply limiting who can view raw borrower detail.

Make outreach safe, consistent, and consent-first

Consent record gates outreach and keeps message proof

Consent record gates outreach and keeps message proof

Automated borrower outreach typically delivers value only when compliance artifacts remain as solid as the productivity gains. TCPA sensitivity, channel permissions, and opt-out handling shape what messaging automation can represent in a mortgage context, and inconsistency across SMS, email, and phone can create reputational and regulatory risk. A consent-first model tends to treat permission and preference as durable data assets, paired with communication records that enable post-hoc review of what was sent, when it was sent, and why it was permitted.

Consent capture and preferences

Consent handling generally centers on channel-specific permission, timestamped records, and a unified view of revocations that propagates across engagement tools. Programs that scale outreach without avoidable friction often treat the consent record as a primary object in CRM/POS, with authority comparable to lead status.

Messaging sequences and proofs

Consistency in messaging commonly relies on approved templates and controlled variants rather than open-ended generation, reducing drift in tone and claims. Proof of outreach typically takes the form of stored message artifacts and activity logs that show content lineage, delivery-attempt history, and any opt-out or preference changes tied to the sequence.

Run a short pilot with human review for exceptions

Short pilots often represent the most credible path to validating ROI in 30–60 days, particularly when executive stakeholders require measurable lift without operational disruption. In mortgage intake and document collection, exceptions occur often enough that human-in-the-loop controls remain central to borrower experience and risk management. Effective pilots commonly emphasize controlled automation for high-volume, low-ambiguity interactions, while preserving human review for uncertainty, regulated edge cases, or situations where incorrect guidance would create downstream rework or compliance exposure.

Human review for edge cases

Exception handling tends to focus on uncertainty thresholds, incomplete applications, and conflicting borrower-provided information, where automated guidance can become unsafe. Human review constructs typically function as safety valves that maintain service standards and lower the probability of misguidance, especially during eligibility triage and sensitive communications.

Keep CRM/POS updated throughout

Operational reliability usually depends on activity normalization back to CRM/POS, where teams expect to see outreach touches, consent updates, document requests, and status changes in familiar timelines. Write-backs act as the connective tissue between digital outreach and internal accountability, and they often determine whether pilot results read as defensible to operations leaders and auditors.