Alex Fesak

CEO

Modern Data Stack for eCommerce Margin & Inventory Accuracy: Reference Architecture for Near-Real-Time COGS, Returns, and Multi-Warehouse Reporting

2026-05-19

Spot margin and inventory mismatches across Shopify, ERP, WMS, and 3PLs

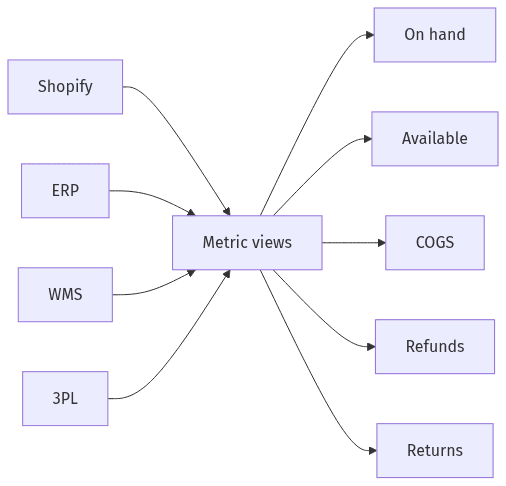

Where key commerce metrics diverge by system

Where key commerce metrics diverge by system

Margin and inventory disagreements typically originate in the seams between systems that record different “truths” on different clocks. Shopify reflects customer-facing order, fulfillment, and refund states, while ERP and WMS/3PL data is anchored to financial posting and physical movements, including backdated adjustments. Across many commerce operations, “stock on hand,” “available to sell,” and “reserved” are calculated differently by platform, and COGS reflects posting conventions and cutoffs rather than a single universal value. Over time, these divergences show up as phantom inventory, close-period restatements, and declining confidence in dashboard numbers.

Quick symptoms to verify first

Early warning signals commonly include missing or duplicated fulfillment events, out-of-order updates, and inconsistent identifiers across order_id, sku, and location_id. Negative inventory at a warehouse, unexplained stock swings after cycle counts, and margin shifts after refunds post often indicate snapshot-oriented reporting and incomplete event history. Gaps between ERP COGS and ecommerce margin frequently trace to timing cutoffs and partial refunds that do not align cleanly to order lines.

Agree on the single source for each metric

Ambiguity around metric ownership routinely creates parallel ledgers. Stock quantities may be treated as WMS-led for operations, while Finance expects ERP tie-outs, and Shopify remains the reference for customer transactions. Explicit system-of-record boundaries for costs, refunds, returns, and inventory states usually reduce reconciliation debate, because mismatches can be evaluated as mapping, timing, or posting differences rather than subjective definitions.

A simple reporting flow for near-real-time operations and finance

From platform updates to trusted reporting tables

From platform updates to trusted reporting tables

Near-real-time reporting holds up better when raw platform feeds are treated as an append-only history instead of mutable snapshots. That orientation supports replayability, clearer audit trails, and tolerance for late-arriving events such as backdated inventory adjustments or delayed return receipts. A common data stack pattern centers a cloud warehouse such as Snowflake or BigQuery, with transformations in dbt producing defined facts for operational and financial views. The material tradeoff remains latency versus correctness, particularly when financial close cutoffs collide with operational urgency.

Bring core updates together from each platform

The core updates typically span orders, fulfillments, shipments, refunds, returns, and inventory movements across multi-warehouse operations and 3PLs. An append-only event log reduces dependence on “current state” API responses that overwrite history, and idempotent handling limits the impact of retries and duplicates. Executive stakeholders often value the resulting audit trail as much as the speed.

Organize reporting tables from raw to trusted metrics

Reporting layers commonly progress from raw ingested tables to standardized entities, then to business-ready facts and marts. Modular dbt models and tests make business definitions inspectable and reduce the fragility of ad hoc SQL. This structure also separates volatile integration behavior from stable metric computation, which becomes more consequential as accuracy expectations tighten.

Accurate multi-warehouse inventory and margin reporting

Multi-warehouse accuracy generally depends on representing inventory as movements over time rather than periodic snapshots that obscure causality. A movement-led approach supports transfers, adjustments, and cycle counts while preserving a reviewable change history at the SKU-location-time grain. Margin accuracy is usually contingent on consistent attribution of COGS, landed cost, shipping costs, duties, and reversals from refunds and returns to the same transaction grain, typically the order line. Without that alignment, returns and partial refunds tend to distort gross profit and sustain disputes between Ops and Finance.

Track inventory changes as a clear, reviewable history

Receipts, picks, transfers, adjustments, cycle counts, and restocks frequently arrive from different systems and at different times, with semantics that vary by provider. A ledger-like history clarifies which event shifted stock and where, supporting multi-warehouse balancing and surfacing gaps such as missing fulfillment decrements. This approach often reduces phantom inventory by making inconsistencies observable rather than averaged away.

Include shipping costs and returns in margin views

Margin volatility often reflects cost and reversal data arriving after the sale, especially with returns timing, condition-based restocking, and carrier charges. Attribution back to the original sale generally reduces confusion when partial refunds occur and when exchanges change the relationship between revenue and physical units. Finance-grade reporting typically depends on consistent treatment of these reversals, rather than recording refunds as simple negative revenue.

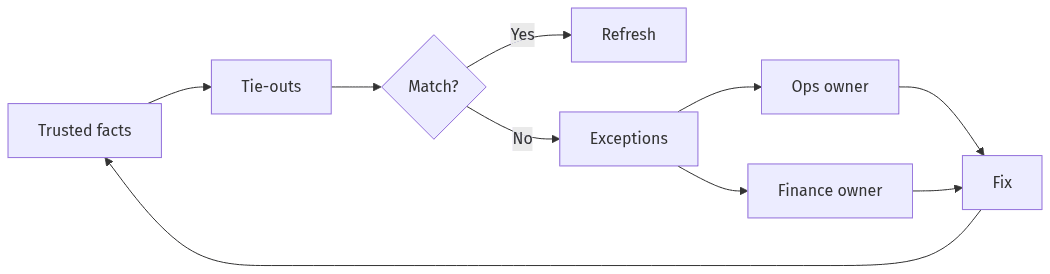

Ongoing tie-outs to keep reports reliable over time

Tie-outs surface exceptions and stabilize reporting over time

Tie-outs surface exceptions and stabilize reporting over time

Reporting reliability tends to erode without ongoing reconciliation, because upstream platforms change schemas, emit duplicates, or introduce latency during peak periods. Cross-system tie-outs act as guardrails, anchoring derived metrics to platform totals and surfacing drift early. More resilient programs treat reconciliation as an operating requirement rather than a one-time milestone, especially for month-end close stability. In ecommerce environments with frequent adjustments and returns, those tie-outs often separate confident decisioning from persistent questioning of the numbers.

Key checks that should always balance

Balancing expectations usually include order and order-line counts against Shopify states, refund totals against payment and finance postings, and inventory-movement sums against warehouse stock positions by location. Negative inventory, unexpected spikes in adjustments, and gaps in fulfillment events often serve as high-signal indicators. Freshness, volume, schema, and anomaly dimensions from data quality standards frequently underpin these controls.

A shared process for investigating exceptions

Exception handling typically breaks down when mismatches lack an owner and when Ops and Finance interpret the same variance through different definitions. A shared view of exceptions across system-of-record boundaries tends to reduce cycle time and prevent recurring debates about whether a metric is “wrong” versus “late.” Auditability also supports compliance expectations around change history and selective exposure of customer data.

Handle late updates to avoid recurring reporting surprises

Late-arriving data is a structural feature of ecommerce operations, not an edge case, particularly with backdated COGS postings, delayed carrier invoices, and returns processed days after delivery. Reporting stability usually comes from explicit restatement expectations rather than optimistic assumptions about timeliness. Executives often prioritize predictable close behavior and trustworthy operational dashboards, even when that requires controlled revisions within defined windows. A near-real-time posture remains compatible with finance-grade reporting when latency, restatements, and audit trails are treated as design constraints.

Rules for late changes and corrections

Restatement policies commonly distinguish between operational views that tolerate ongoing updates and financial views that require period stability. Watermark-style boundaries and limited reprocessing windows often shape how far back metrics can move, while correction logic preserves auditability for adjustments and backdated transactions. The core tension typically shows up as correctness versus immediacy, rather than a purely technical limitation.

Basic monitoring to catch issues early

Monitoring usually focuses on missing updates, unusual changes in key totals, and drift between sources and warehouse facts. Alerts frequently align to freshness and volume signals, schema shifts, and anomalies in inventory movements or refunds, because those patterns correlate with phantom inventory and margin surprises. Observability supports executive confidence by turning silent failures into visible, time-bounded incidents.